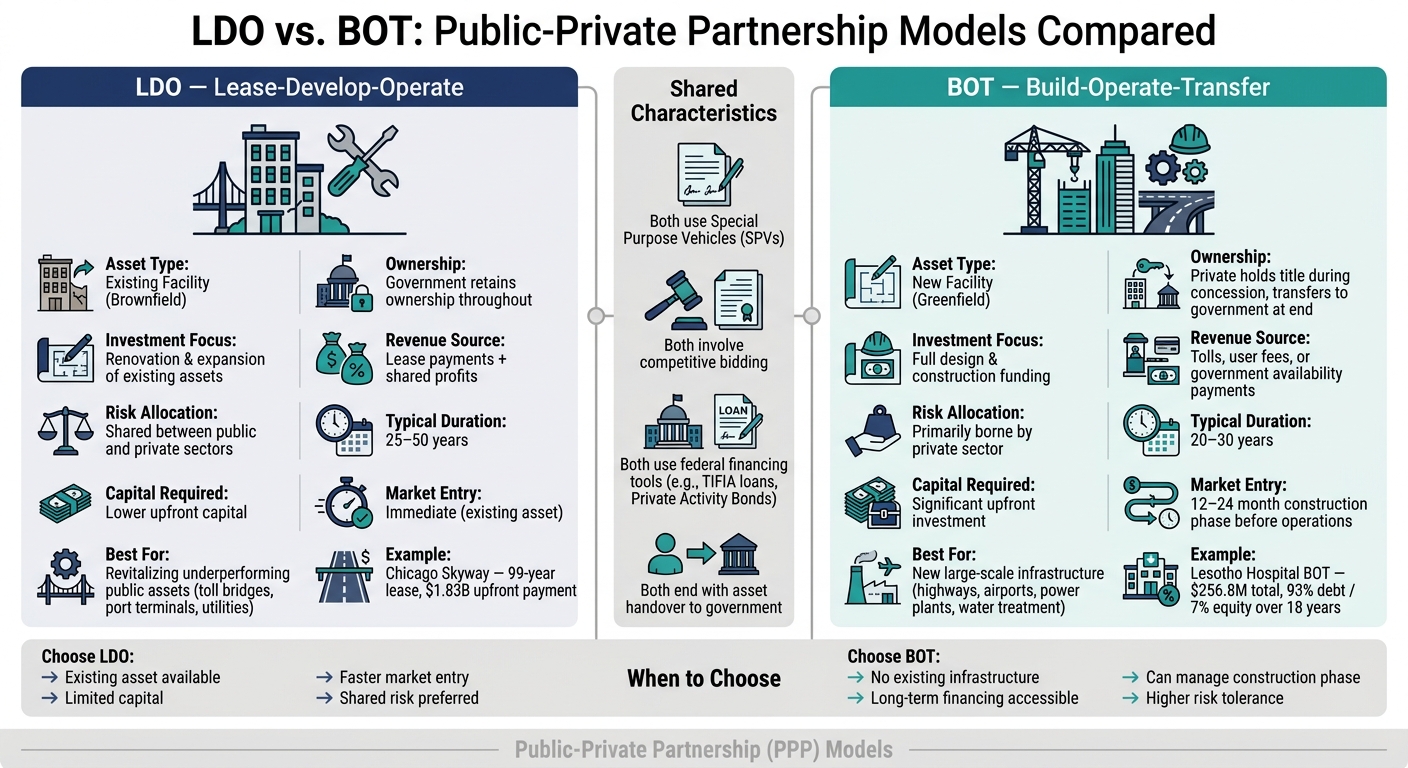

LDO (Lease-Develop-Operate) and BOT (Build-Operate-Transfer) are two public-private partnership (PPP) models used for infrastructure projects. The key difference? LDO focuses on upgrading and managing existing assets (brownfield projects), while BOT is used to build new infrastructure (greenfield projects). Here's a quick breakdown:

- LDO: Government leases an existing asset to a private partner for development and operation. Ownership remains with the government.

- BOT: A private partner finances, builds, and operates new infrastructure, transferring ownership to the government after the contract ends.

- Risk: LDO involves shared risk, while BOT places more risk on the private partner (e.g., construction and revenue risks).

- Financing: LDO projects usually require less upfront capital compared to BOT, which involves significant investment.

- Use Cases: LDO suits projects like toll bridges or utility upgrades; BOT is ideal for highways, airports, or power plants.

Quick Comparison

| Feature | LDO (Lease-Develop-Operate) | BOT (Build-Operate-Transfer) |

|---|---|---|

| Asset Type | Existing (Brownfield) | New (Greenfield) |

| Ownership | Public retains ownership | Private holds title temporarily |

| Investment Focus | Renovation/expansion | Full construction funding |

| Revenue Source | Lease payments, shared profits | Tolls, user fees, government |

| Risk Allocation | Shared | Private bears most risks |

| Typical Duration | 25–50 years | 20–30 years |

Choosing between LDO and BOT depends on your goals, financial capacity, and risk appetite. If you’re working with existing assets, LDO might be the better fit. For new infrastructure, BOT offers a structured path to execution.

LDO vs. BOT: Public-Private Partnership Models Compared

How the Lease-Develop-Operate (LDO) Model Works

Definition and Core Features

The Lease-Develop-Operate (LDO) model involves a government agency leasing a public asset - along with its associated land - to a private partner for a set period. Ownership of the asset remains with the government, while the private partner gains a leasehold interest and pays a lease fee. This model is primarily applied to brownfield assets, which are existing infrastructure projects like toll bridges, port terminals, or utility facilities that are already in use. The private partner is responsible for improving, expanding, and managing the asset while adhering to the terms of the agreement. The process unfolds in a structured manner, moving from leasing to eventual handover.

Lifecycle and Contract Structure

The LDO model operates through a clear lifecycle: leasing, development, operation, and handover. Public authorities typically award these contracts through competitive bidding, evaluating factors like financial stability and relevant expertise. Once the lease is secured, the private partner invests in upgrades and begins operating the asset. During the operational phase, the private entity manages day-to-day activities, collects revenue, and pays lease fees to the government. Performance is monitored against agreed standards, with penalties for non-compliance. At the end of the lease term, the asset is handed back to the government in a condition specified in the contract.

Lease durations under this model often range from 25 to 50 years, though some agreements extend further. For instance, the City of Chicago leased the Chicago Skyway toll bridge to a consortium led by Macquarie and Cintra for 99 years in exchange for an upfront payment of $1.83 billion. The contract included a toll escalation schedule tied to the Consumer Price Index (CPI). In 2016, the lease was resold to IFM Investors at a higher valuation. Lease fee structures can differ based on the asset and agreement, commonly taking forms such as fixed annual rent per square foot, a lump sum combined with a variable share of cash flow, or a royalty-style arrangement blending fixed and revenue-based payments.

Risk Allocation and Financing

In LDO arrangements, risk is divided between the public and private partners. The private partner typically assumes risks related to traffic, revenue, operations, maintenance, and capital improvements. Meanwhile, the public partner retains ownership, gains upfront liquidity, and may provide minimum revenue guarantees during the early years to reduce the private partner's financial exposure.

Financing for LDO projects often involves private equity, Private Activity Bonds (PABs), and federal programs like TIFIA loans. These deals are generally structured through a Special Purpose Vehicle (SPV) to manage risk.

The Indiana Toll Road deal illustrates the risks of overly aggressive financing. In 2006, a Macquarie-Ferrovial consortium paid $3.85 billion for a 75-year lease on the 157-mile road, structured with a debt-to-EBITDA ratio of 6:1. Following the 2008 recession, traffic dropped by 15–20%, leading the operator to file for bankruptcy in 2014. IFM Investors later acquired the lease for $5.725 billion after debt restructuring and traffic stabilization. Today, LDO deals aim for more conservative debt-to-EBITDA ratios of 4:1 to 5:1 to avoid similar financial pitfalls.

sbb-itb-01010c0

How the Build-Operate-Transfer (BOT) Model Works

Definition and Core Features

The Build-Operate-Transfer (BOT) model is a public–private partnership where a private company takes on the responsibility of financing, building, and operating an infrastructure project for a set period - usually between 25 to 50 years. Once the contract ends, the ownership transfers back to the government. Unlike Lease-Develop-Operate (LDO) models, which focus on existing infrastructure, BOT is specifically designed for creating new projects. These are often referred to as "greenfield projects" and include ventures like highways, power plants, airports, and wastewater treatment facilities. Without BOT, such projects are typically funded entirely by public resources.

A key feature of the BOT model is the creation of a Special Purpose Vehicle (SPV) by the private consortium involved. This consortium, which often includes construction firms, infrastructure investors, and operators, uses the SPV to manage the project. The SPV ensures that financial risks are kept separate from the parent companies' balance sheets. To recover their investment, the private partner relies on mechanisms like tolls, utility fees, or government payments based on availability. This structured approach provides a clear framework for understanding how BOT projects are managed and how risks are shared.

Lifecycle and Contract Structure

A BOT project unfolds through four distinct phases: concession award, design and construction, operation and maintenance, and transfer. After a competitive bidding process, the selected private partner secures financing and begins designing and constructing the project. During this phase, the private entity takes on all construction-related risks, such as delays or cost overruns. Once the project becomes operational, the private partner is responsible for managing the facility according to performance standards outlined in the contract. At the end of the agreed term, the asset is handed back to the government in a pre-determined condition.

"The advantage of the DBOM [BOT] approach is that it combines responsibility for functions that are usually disparate - design, construction, and maintenance - under a single entity." - FHWA Center for Innovative Finance Support

A great example of this integrated approach is the Hudson-Bergen Light Rail project in New Jersey. This project used a Design-Build-Operate-Maintain (DBOM) structure, which is functionally similar to BOT. By combining long-term maintenance considerations into the design phase, the private partner was able to lower overall lifecycle costs compared to traditional procurement methods.

Risk Allocation and Financing

Risk allocation in BOT projects is notably different from models like LDO. During the design and operational phases, the private company assumes a significant portion of the risk. This includes managing potential construction delays, cost overruns, and site-related challenges. In cases where user-pay mechanisms (like tolls or fares) are used, the private partner also bears the risk of revenue shortfalls if actual demand falls below projections.

The Bangkok Mass Transit System (BTS) Skytrain serves as a cautionary example. In the 1990s, the Bangkok Metropolitan Administration awarded a 30-year BOT concession to Bangkok Mass Transit System Public Company Limited (BMTS). BMTS anticipated recovering its costs within 10 years, based on a projected 16% return. However, ridership numbers fell far short of expectations, leading to severe financial difficulties for the company.

Financing for BOT projects often relies on limited-recourse loans, meaning lenders can only claim against the SPV's assets and revenues. Federal programs like TIFIA can step in to cover up to 33% of eligible project costs, providing additional financial support. Moreover, agreements like Power Purchase Agreements (PPAs) can guarantee minimum revenue levels, helping to offset demand risks.

LDO vs. BOT: Key Differences

Side-by-Side Feature Comparison

The main distinction between LDO and BOT lies in the origin of the asset. LDO focuses on existing facilities - referred to as brownfield projects - that require upgrades or improved management. On the other hand, BOT is tailored for greenfield projects, which involve building entirely new infrastructure. These differences in asset origin, along with variations in ownership and investment needs, directly influence which model is most suitable.

| Feature | Lease-Develop-Operate (LDO) | Build-Operate-Transfer (BOT) |

|---|---|---|

| Asset Origin | Existing facility (Brownfield) | New facility (Greenfield) |

| Ownership During Contract | Government retains ownership | Private entity holds title during the concession and transfers it to the government later |

| Investment Requirements | Renovation and expansion of existing assets | Full design and construction of new assets |

| Revenue Source | Shared profits and lease payments | Tolls, user fees, or government agreements |

| Risk Allocation | Shared between public and private sectors | Primarily borne by the private sector |

| Typical Contract Duration | Based on agreed lease term | Typically 20–30 years |

Risk Profiles and Financial Considerations

In a BOT model, the private partner assumes a significant share of the risk. This includes financing construction, managing potential delays, and handling revenue shortfalls. A notable example is the Lesotho national referral hospital BOT project, initiated in October 2008. It involved a total investment of US$256.8 million over 18 years, with the private consortium’s financing structured as 93.01% debt (US$142.4 million) and 6.99% equity (US$10.7 million). This high debt-to-equity ratio highlights the financial intensity of BOT projects, where potential returns - and losses - are magnified.

LDO projects, by contrast, present lower risks for private operators. Since the asset is already in place, uncertainties tied to construction are largely avoided. Additionally, the government retains ownership throughout the lease period, and revenue is typically shared. This makes LDO an appealing choice for private entities looking to avoid the full risks associated with greenfield developments. These contrasting risk profiles influence where each model is most effectively applied.

Use Cases and Sector Applications

The differences in financial and risk characteristics make LDO and BOT suitable for specific types of projects. BOT is commonly used for large-scale infrastructure projects such as highways, power plants, airports, and water treatment facilities. These projects are ideal for situations where governments need new infrastructure but lack the funds to build it independently.

On the other hand, LDO is better suited for revitalizing underperforming government-owned assets. Examples include transport yards, utilities, and public buildings. Governments turn to LDO arrangements to bring in private expertise while maintaining ownership of these assets.

In the U.S., the choice between LDO and BOT often depends on the state of existing infrastructure and financial constraints at various levels of government. LDO is a practical option when public agencies aim to improve and monetize assets they already own. Meanwhile, BOT is a go-to solution when there’s a need to create new infrastructure but public funding is limited, making private investment essential.

Choosing Between LDO and BOT for Market Expansion

Decision Criteria and Framework

When deciding between an LDO (Lease, Develop, Operate) model and a BOT (Build, Operate, Transfer) model for market expansion, the choice often depends on your financial position, timeline, and risk appetite.

An LDO model is ideal if you aim to revitalize an existing asset with limited initial investment while maintaining a balanced risk profile. On the other hand, BOT is better suited for situations where building new infrastructure is feasible and long-term financing is accessible.

LDO arrangements allow for quicker market entry since revenue generation begins immediately from existing assets. In contrast, BOT projects typically involve a 12–24 month construction phase before operations can commence. Early sensitivity analysis is critical for both models, factoring in inflation, fee escalations, and potential penalties. The high debt requirements in BOT projects make this analysis even more essential, as they can significantly amplify risks.

Here’s a quick comparison to guide your decision:

| Decision Factor | Choose LDO | Choose BOT |

|---|---|---|

| Asset availability | Existing facility ready for use | No suitable infrastructure exists |

| Capital position | Limited upfront capital | Access to long-term debt financing |

| Timeline | Need faster market entry | Can manage a 12–24 month build phase |

| Risk tolerance | Prefer shared risk | Can handle primary construction/revenue risk |

| Ownership goal | Government retains ownership | Private entity holds title during concession |

To ensure your choice aligns with your goals, use robust analytical tools and seek expert advice to validate your model.

Using Analytical Tools and Advisory Support

Making an informed decision requires a thorough evaluation of market size, potential risks, and revenue projections. Tools like the Market Entry Navigator from The B2B Ecosystem can help craft tailored market entry strategies by considering factors like capital constraints, regulatory environments, and long-term ownership goals.

For financial modeling, the TAM Analyst tool is particularly useful. It breaks down market size into actionable segments - TAM (Total Addressable Market), SAM (Serviceable Addressable Market), and SOM (Serviceable Obtainable Market). This segmentation is crucial for assessing the revenue potential of BOT projects under varying demand scenarios. Complementing this, the Risk Analyzer applies automated risk scoring based on financial and market data, providing a structured method to stress-test your model before committing to a long-term contract.

"The BOT model gives companies a practical way to grow with control and confidence." - Dmitry Nazarevich, CTO, Innowise

Additionally, advisory support is indispensable when navigating regulatory challenges. Markets with complex compliance requirements - such as foreign investment rules, environmental clearances, or public procurement laws - demand expert guidance. This expertise can help avoid costly mistakes during the contract structuring phase, ensuring smoother transitions and renewals down the line.

Conclusion

LDO focuses on upgrading and managing existing public assets, while BOT is all about creating brand-new infrastructure. LDO is tailored for brownfield projects - where public assets are modernized and operated by private entities, but ownership remains with the government. BOT, on the other hand, is for greenfield projects, where private capital funds the construction of new infrastructure, typically under a 20–30 year concession, before handing it back to the public sector.

These models don’t just differ in purpose - they also come with distinct financial and operational considerations. BOT requires significant upfront investment and places the burden of construction and demand risks on the private partner. LDO, however, involves a lower initial cost and emphasizes a shared approach to risks and profits, making it a more feasible option for companies with limited financial resources.

As UBR Infra aptly puts it:

"Start with clear objectives, assess risk, choose the model aligned with your strengths, and build sustainable, high-quality infrastructure." - UBR Infra

To ensure a successful partnership, align your PPP model with your business goals, considering factors like capital availability, timeline, risk tolerance, and desired ownership structure. Resources such as the Market Entry Navigator and Risk Analyzer from The B2B Ecosystem can help you refine your strategy. These tools can validate assumptions, estimate market potential through TAM/SAM/SOM segmentation, and provide automated risk scoring before entering into a long-term commitment.

Whether you're looking at an LDO setup to revitalize an existing asset or planning a BOT deal for a new project, having a solid analytical framework and expert guidance can make all the difference.

FAQs

How do I decide between LDO and BOT for my project?

Choosing between Lease-Develop-Operate (LDO) and Build-Operate-Transfer (BOT) hinges on the specific requirements of your project.

LDO works well when you need to upgrade or expand existing facilities without taking on the full cost of ownership. On the other hand, BOT is better suited for large-scale, new infrastructure projects where a private entity handles construction, manages operations, and later transfers ownership back to the public or another party.

Key factors like your budget, the scope of the project, and the current condition of the assets will help determine which model is the better fit for your objectives.

What are the biggest risks private partners face in BOT deals?

Private partners involved in Build-Operate-Transfer (BOT) agreements encounter several challenges. Construction risks often top the list, including unexpected cost overruns, delays in project timelines, or unforeseen site conditions. Beyond this, regulatory risks - like changes in tax policies or updated safety standards - can significantly impact project viability.

Another major concern is revenue risk, often tied to consumer tariffs, which can fluctuate and affect profitability. Then there's the matter of operational risks, where penalties may be imposed if performance benchmarks aren't met.

To navigate these hurdles, conducting thorough due diligence and seeking professional guidance is crucial. These steps help ensure risks are identified, allocated, and managed as effectively as possible.

How are LDO and BOT contracts typically financed in the U.S.?

In the U.S., Build-Operate-Transfer (BOT) projects are typically financed using project finance structures. This approach blends equity contributions from private partners with debt provided by financial institutions. The terms of these agreements are customized based on projected cash flows, often including grace periods to account for the construction phase.

On the other hand, Lease-Develop-Operate (LDO) contracts focus on using private capital to upgrade or modernize public facilities. These agreements involve a shared risk model, where private entities recoup their investments through operational revenues.

Both BOT and LDO models gain strategic and operational support from resources like The B2B Ecosystem, which helps streamline planning and execution.